10: The Stock Swindle Part 2: After The Fall

By the end of Stillson’s speech, even if the viewer doesn’t fully understand all of his financial jargon, the speech does manage to communicate that Hudsucker Industries is indeed doing very very well as a company, if for no other reason than the speech being capped off by “In short: we’re loaded”

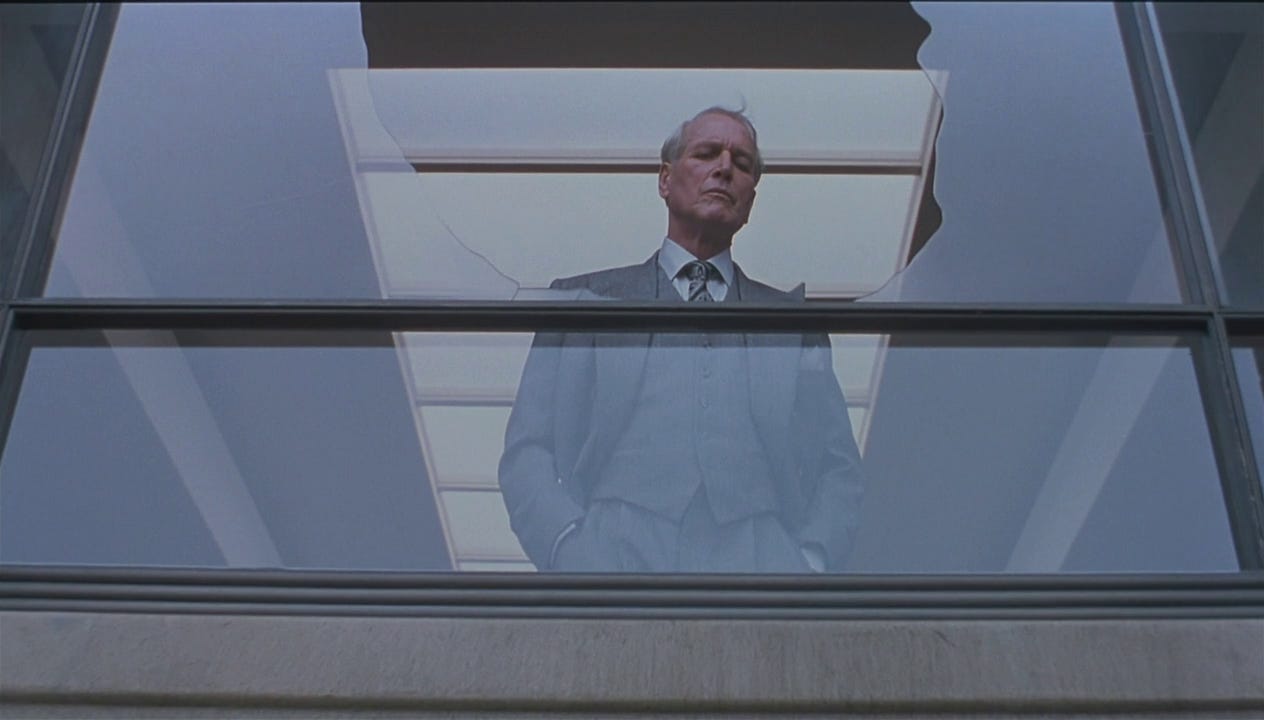

As the board laughs at his absolutely comical use of the english of the hoi polloi, Waring Hudsucker clears his throat, winds his watch, takes a puff of his cigar, climbs up on the boardroom meeting table, and jumps out the window, plummeting 45 floors (counting the mezzanine) to his demise. Exactly 1 minute and 30 seconds after Stillson announces that the company is loaded, this statement goes from good news to very bad news.

The macguffin that moves the plot of the film is that the Hudsucker board and especially its Senior Vice President, Sidney Mussburger, are powerful men who wish to remain powerful. They understand in a very intimate way the status of their company and do not wish to risk the sweet gig they have found themselves with. They understand that in the long term running Hudsucker Industries is going to be a very lucrative job, but more than that, they understand that it’s a powerful position. Within minutes of Waring Hudsucker’s death, probably before an ambulance has arrived to confirm he’s even dead, the Hudsucker board has agreed to commit securities fraud, lowering the value of Hudsucker Industries stock, and thus their own net worth in order to maintain control of the company. Much as some late ancien régime French nobility saw their finances ruined and thus their estates crumble rather than show that they would deign to perform labor of any kind or renounce their aristocratic titles, so to do the Hudsucker board value their titles and associated privilege above mere finances.

The puzzling question though is: is this even possible? At the time of his demise, Waring Hudsucker owned 87 percent of Hudsucker’s stock. There are 18 people in the Hudsucker board room at the beginning of the film (19 counting Hudsucker himself). Those 18 people would not need to collectively own all of Waring Hudsucker’s 87 percent of the company’s stock to retain control of the company however, only just over 50 percent, just enough to keep anyone else from owning a majority of the company. So how much money would Hudsucker Industries have to lose in value and how much would those 18 men have to spend to maintain control of the company?

First, how much is Hudsucker worth? It’s tough to value a fictitious company, but one gets the sense that Hudsucker is a giant corporation at the height of its powers after a long run of its initial founder’s control. We also get the sense that due to the number of subsidiaries and franchises it controls along with its giant manufacturing apparatus that this is a company with a nationwide presence (with some international presence as well) that potentially touches hundreds of millions of lives. An example of a company similar to this springs to mind: The Ford Motor Company of Detroit Michigan.

Henry Ford established the Ford Motor Company (the third automotive company that Ford founded, but ultimately the one that stuck around with his name still attached to it) in 1903 with an investment of $28,000. After that point in Ford's life as with Waring Hudsucker’s, he built the company up from his bare hands; every step he took was a step up. While Henry Ford had left day to day operations in the early 1940s and died in 1947, when the company made its initial public offering in 1956, his family retained control of 40 percent of the company selling the remainder as common stock for a market capitalization of $660 million. If Ford had similar bylaws to Hudsucker and the 40% family ownership were turned into common stock in the event of tragedy, this would place the market capitalization and thus value of the company in total at $1.1 billion total.

The total value of the biggest corporations in the world appear to hover at around the single digits of the billion dollar place for most of the 1950s. General Motors was worth $10 billion in 1958 when the film was set and was the biggest company in the world at that point. The 5th biggest company was General Electric, valued at $4 billion. Once again, we do not know where Hudsucker ranks historically in terms of corporate size as it never existed, but we do have a hint. Hudsucker Industries is headquartered in a 44 floor (45 counting the mezzanine) Madison Ave skyscraper in the middle of Midtown Manhattan.

In the meantime, in the real world, one of Manhattan’s most iconic structures the Chrysler Building was built as a headquarters for the Chrysler corporation in 1931 and comprises 70 floors in the heart of Midtown Manhattan.

The Hudsucker Building is then 65% the size of the Chrysler building. If an apples to apples comparison can be made, this would make Hudsucker roughly 65% as big of a company as Chrysler. In 1958 Chrysler was valued at $3.5 billion. 65% of $3.5 billion is $2.7 billion, putting Hudsucker Industries at around the same size as AT&T in 1958. It’s entirely reasonable then to assume that Hudsucker Industries is worth between $1 and $3 billion at the time of Waring Hudsucker’s death.

Before we go any further, a quick note on how stocks and stock trading works: In a perfect world, a stock represents an individual tiny piece of the value of all of a company’s assets without any of its liabilities. If I formed a company tomorrow called O’Brien’s Mining Concern whose sole corporate asset is one $10 pickaxe and nothing else, and I issue 1,000 shares of stock in that company, each of those shares would be worth exactly one penny, being 1/1000th of $10. If however O’Brien’s Mining Concern then digs up a diamond valued at $990, it now owns $1,000 worth of assets (a $990 diamond and a $10 pickaxe), and each one of those 1,000 shares is now worth $1. In the real world, however, companies are substantially more complex entities than things that own one pickaxe and one diamond. While publicly traded companies are regularly valued via rigorous internal auditing, a great deal of what determines a stock’s price is the public’s conception of it. Outside sudden diamond-based windfalls, it’s profoundly difficult for a company to create $13 billion in value over the course of 30 days, and yet that’s exactly what happened to Apple 30 days after announcing the original iPhone. In this instance in the immediate aftermath of the announcement of the iPhone, more people wanted to buy Apple stock than people wanted to sell it, so in order to be able to purchase the stock the folks who wanted to buy it needed to offer a higher price to entice the people who had it to sell, and that difference on paper made Apple worth $13 billion more than it had previously. This difference between public confidence and actual value is what Mussburger is hoping will happen to Hudsucker to his advantage. Over the course of the month of December 1958, Hudsucker will retain more or less the same amount of factories, offices, employees, and inventory of wingdings and gizmos to sell, but if the company looks bad, Waring Hudsucker’s shares will sell for way less than what they’re actually worth, allowing Mussburger and his cronies to keep their jobs.

If we assume Hudsucker’s value at $1 billion, in order to own a majority of the company the board would need to purchase $500 million worth of stock. The board of course can’t afford this, hence the securities fraud. What, though, can they afford? We do not know exactly how wealthy or not these men are, but we do have a hint. After the Hula Hoop is a massive success, a scene in the Hudsucker boardroom opens with a board member with spectacular eyebrows named Addison wailing as he has learned that Mussburger had sold all the board’s stock in an attempt to further depreciate the price. “I had twenty thousand shares! I’d be a millionaire now!” he blubbers.

“Sure sure, we’d all be millionaires”, Mussburger responds. The phrases “I’d be a millionaire” and “we’d all be millionaires” suggests that not only is Addison not a millionaire, but in fact that the majority of the Hudsucker board are not either. Even if some of the board are millionaires and others aren’t, the best we can hope for their collective net worth is around $18 million. It would take all of them pawning literally everything they’re worth to raise enough capital to purchase a little under 2% of the company. In order to take control of the company, its total value would need to drop from $1 billion (that is to say $1,000 million) to $36 million, which would give the Hudsucker board the ability to purchase the barest majority of the company with their $18 million in net worth. Is it even possible to depress the stock via PR and phoney leadership alone to get it to 1/28th of its value in one month?

One of the greatest stock crashes within living memory was the 2008 financial crisis. The first domino that fell starting the crisis was the demise of Lehman Brothers Financial in 2007. The public realized that the banking magnate did not have sufficient capital to cover its outstanding debts, and could not capitalize on the many many subprime loans it had made, including a category of loans called “NINA” loans, an acronym for “No Income No Asset” loans. If you think a large bank loan given to someone with no income and no assets is a bad idea, the world in 2007 agreed, driving Lehman’s stock from its height of $70 per share down to a low of $7.79 when they declared bankruptcy, starting the cascading reaction that ultimately became the 2008 financial crisis. Lehman dropped to 1/9th of its value incredibly quickly, commonly considered to be one of the greatest boondoggles in stock market history. However it did not drop in a single month. It dropped from its height in January 2007 to bankruptcy levels in September of the same year.

An even bigger corporate scandal of the 21st century happened right as it began. After several years of steady growth and being called “America’s Most Innovative Company” by Fortune Magazine, Enron stock traded at an average of $64 per share for most of 2000. In 2001 however its stock began dropping as it became more and more apparent that any and all appearance on paper of its value turned out to be a complicated instance of financial shadow puppetry. As its CEO Kenneth Lay began selling his shares of stock while insisting to his employees and shareholders that the company was doing swell the stock price started to slip. By September of 2001 he told his employees that the company’s accounting methods were “legal and totally appropriate”, which is a normal thing for a company whose accounting methods are legal and totally appropriate to say.

Soon after the company posted a $618 million loss, had its finances investigated by the SEC, and ultimately filed for bankruptcy as its stock was trading for $0.21 in December of 2001. While Enron succeeded in completely destroying its perceived value in the eyes of the public, it took the better part of a calendar year to do. Not even Kenneth Lay could drop their stock to 3.8% of its initial value in a month.

Stocks can also be devalued due to bad PR and loss of public trust. One of the worst single month drops in stock in recent history regards the German auto manufacturer Volkswagen. When Volskwagen admitted in September of 2015 that it had been faking emissions data to violate the US Clean Air Act for the past 7 years, its stock took a massive plummet, but it did not drop to 1/28th of its initial value. It dropped to roughly ¾ of its value by the end of the month.

Ultimately though what the Hudsucker board is hoping will happen is that the public will lose faith in Hudsucker due to its poor public facing leadership. Once again we have a real world example of exactly that. Over the course of the second half of 2018 as “visionary” maverick CEO of Tesla Elon Musk burned his public goodwill in a fire by first announcing an upcoming “joke” flamethrower company, then calling a diver rescuing a trapped Thai Boys Soccer team a “peco guy” after the internet ridiculed his mini submarine rescue idea, then pretending to smoke weed on the Joe Rogan Experience podcast, and then ultimately committing actual literal securities fraud by announcing that he was planning on taking Tesla private at the “hilarious” price of $420.69 per share.

This activity caused Tesla’s stock to drop from $330 in June 2018 to $194, a little over 2/3rds of its initial value in January of 2019. A drop by a third of its value in half a year is once again a far cry from dropping to 1/28th of its initial value in one month.

In terms of a company whose entire idea of value turned out to be a fabrication, it’s difficult to imagine a worse example than Enron in 2001. In terms of corporate malfeasance that destroys public goodwill, it’s difficult to imagine a worse example than Volkswagen’s emission’s cheating. In terms of a CEO personally destroying confidence in the company they’re running, it’s difficult to imagine a more striking example than Musk’s 2018 meltdown. None of them lost nearly enough value to get to 1/28th of its original value, and certainly none of them did it in a month.

As the Hudsucker board imagines their stock swindle a quick chorus of “It would work!”, “It could work!”, “It’s workin’ already!” erupts around the boardroom table. They of course do not count on the fact that their “imbecile” president that they hire would invent one of the most popular toys of the century, but even if their plan had worked perfectly and the public had lost all confidence in the company, the absolute best they could hope for would maybe being able to buy 4% of the company rather than 2%. One gets the sense that Waring Hudsucker may not have hired the best and brightest to run his boardroom after all.